When it comes to building wealth, one principle stands tall above the rest: compound interest. Often called the “eighth wonder of the world,” compound interest has the power to turn small, consistent savings into substantial financial growth over time. But there is one critical factor that determines just how powerful compound interest can be — the age at which a person starts saving.

So, how does the age that a person starts saving impact the amount they can earn in compound interest? The answer is simple yet profound: time magnifies money. The earlier you start, the more time your money has to grow — and growth on growth creates exponential results.

In this detailed guide, we will explore how starting age affects compound interest, compare early and late savers, break down mathematical examples, examine psychological and financial benefits, and explain how anyone — regardless of age — can maximize their savings potential.

What Is Compound Interest and Why Does It Matter?

Before understanding how starting age impacts compound interest, we must first understand what compound interest is. how does the age that a person starts saving impact the amount they can earn in compound interest

Compound interest is the process where interest is earned not only on the original amount invested (principal) but also on the accumulated interest from previous periods.

In simple words:

- You earn interest.

- That interest is added to your total.

- Next time, you earn interest on a bigger total.

This cycle continues and accelerates over time.

The Formula Behind Compound Interest

The compound interest formula is:A=P(1+r/n)nt

Where:

- A = Final amount

- P = Principal (initial investment)

- r = Annual interest rate

- n = Number of times interest compounds per year

- t = Number of years

how does the age that a person starts saving impact the amount they can earn in compound interest Notice something important here — the variable t (time) sits in the exponent. That means time has exponential power, not linear power.

And this is exactly why age matters.

How Does the Age That a Person Starts Saving Impact the Amount They Can Earn in Compound Interest?

The age at which someone begins saving determines how many years their money has to compound. Since compound growth is exponential, every additional year makes a significant difference. how does the age that a person starts saving impact the amount they can earn in compound interest?

Let’s break it down with a real-life style example.

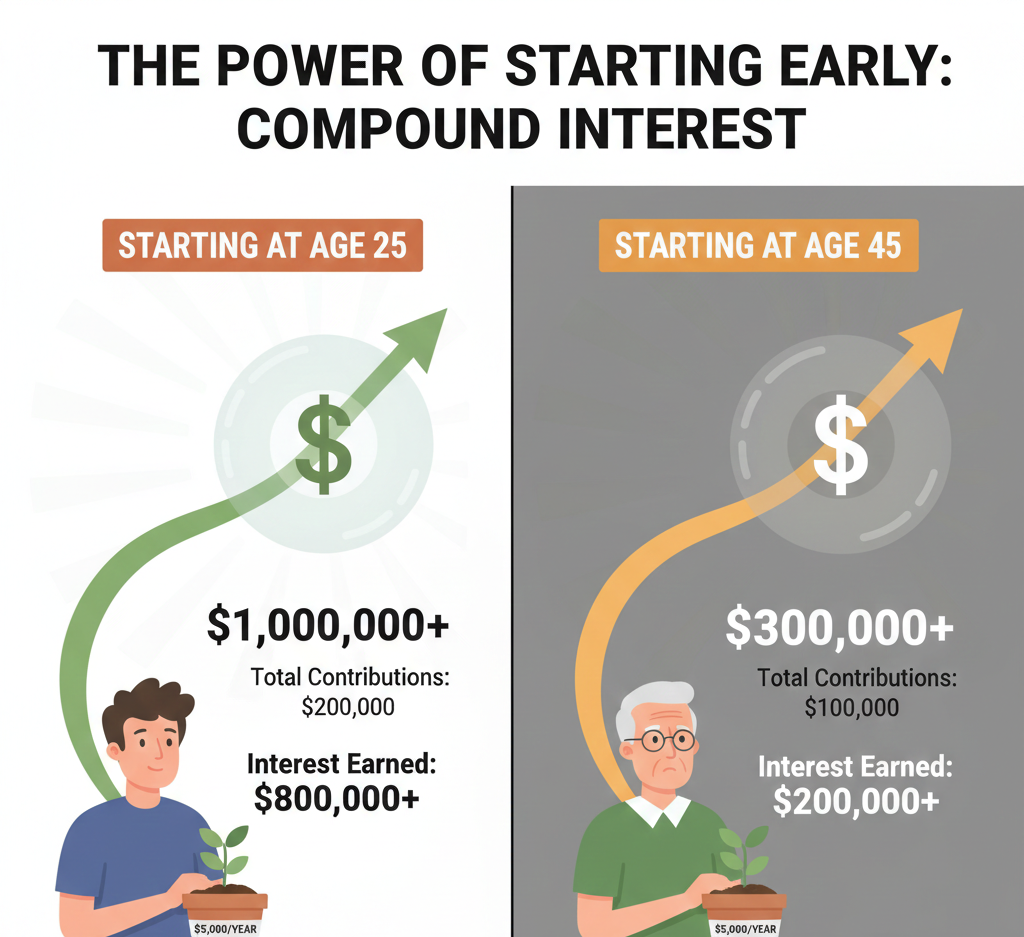

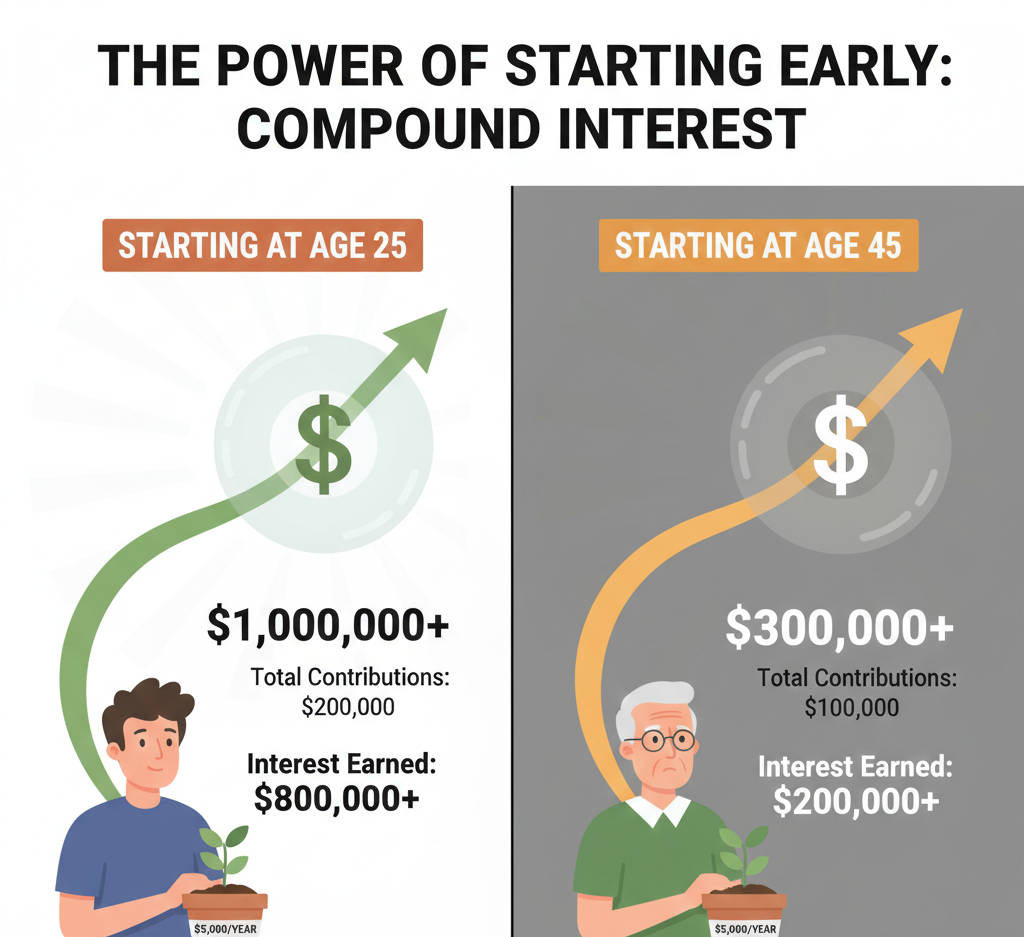

Example 1: Starting at Age 20 vs Age 30

Assume:

- Investment: $5,000 per year

- Annual return: 8%

- Compounded annually

Person A:

- Starts saving at 20

- Saves until 60 (40 years)

Person B:

- Starts saving at 30

- Saves until 60 (30 years)

Even though Person B only started 10 years later, the difference in final wealth is dramatic.

After 40 years at 8%, Person A could accumulate over $1 million.

Person B, saving the same amount but for 30 years, may accumulate around $600,000–$700,000.

That 10-year delay costs hundreds of thousands of dollars.

how does the age that a person starts saving impact the amount they can earn in compound interest This clearly shows how does the age that a person starts saving impact the amount they can earn in compound interest — it can mean the difference between financial freedom and financial stress.

The Power of Time: Why Early Years Matter More Than Later Years

Many people believe saving more later can compensate for not saving early. However, compound interest doesn’t reward intensity — it rewards consistency and time.how does the age that a person starts saving impact the amount they can earn in compound interest

The First 10 Years Are the Most Powerful

If you invest early:

- Your early contributions generate interest.

- That interest generates more interest.

- The compounding effect accelerates over decades.

Interestingly, in long-term investing:

- The last 10 years often produce more growth than the first 20 combined. how does the age that a person starts saving impact the amount they can earn in compound interest

- But that explosive growth only happens if the money was invested early.

Time is like fertile soil. The earlier you plant the seed, the larger the tree grows.

Comparing Early Saver vs Late Saver: A Deeper Financial Breakdown

Let’s consider two individuals:

Early Saver (Emma)

- Starts at age 22

- Saves $300 per month

- Stops at age 32 (only 10 years of saving)

- Leaves money invested until 60

- 8% annual return

Late Saver (Daniel)

- Starts at age 32

- Saves $300 per month

- Continues saving until 60 (28 years)

- Same 8% return

Who ends up with more money?

Surprisingly, Emma — who saved for only 10 years — could end up with more money at retirement than Daniel.

Why?

Because Emma gave her money 38 years to compound, while Daniel gave his money only 28 years.

This perfectly answers the question: how does the age that a person starts saving impact the amount they can earn in compound interest? Even a short early start can outperform decades of late saving.

The Exponential Curve of Compound Growth

Compound interest growth follows an exponential curve.

In early years:

- Growth appears slow.

- Gains seem small.

In later years:

- Growth accelerates dramatically.

- Interest earned becomes larger than annual contributions.

This is why many investors regret not starting earlier. The real magic of compounding happens in the final stretch — but only if you gave it enough time.

The Psychological Impact of Starting Early

Starting to save early doesn’t just grow money — it builds financial discipline.

When someone starts saving young:

- They develop consistent saving habits.

- Investing becomes automatic.

- Risk tolerance may be higher.

- Financial anxiety decreases.

Meanwhile, people who delay saving often:

- Feel pressure to invest aggressively.

- Take higher risks to “catch up.”

- Experience stress about retirement.

So how does the age that a person starts saving impact the amount they can earn in compound interest? It affects not only financial results but also mental peace.

Inflation and Its Role in Long-Term Saving

Another reason why starting early matters is inflation.

how does the age that a person starts saving impact the amount they can earn in compound interest. Inflation reduces purchasing power over time. Money saved later must grow faster just to maintain value.

If inflation averages 3% annually:

- $1 today may be worth only about $0.55 in 20 years.

Starting early gives your money time to outpace inflation.

Retirement Accounts and Compound Interest

Compound interest becomes especially powerful when combined with retirement accounts such as:

- 401(k)

- IRA

- Pension funds

- Mutual funds

These accounts allow money to grow tax-advantaged, further accelerating compound growth .how does the age that a person starts saving impact the amount they can earn in compound interest

The earlier contributions begin, the more powerful tax-deferred compounding becomes.

What If You Start Late? Is It Too Late?

A common question is: “I’m already 35 or 40. Is it too late?”

The answer: It’s never too late — but earlier is better.

If starting late: how does the age that a person starts saving impact the amount they can earn in compound interest.

- Increase monthly contributions.

- Reduce unnecessary expenses.

- Invest consistently.

- Avoid withdrawing early.

While you may not match the results of someone who started at 20, disciplined investing can still build substantial wealth.

Real-Life Scenario: The Cost of Waiting 5 Years

Let’s assume:

- $10,000 invested at 8% annually.

If invested at:

- Age 25 → grows for 35 years.

- Age 30 → grows for 30 years.

The 5-year delay can reduce final wealth by tens of thousands of dollars — even if the initial amount is the same.

Five years may seem short in life, but in compound interest, it’s massive. how does the age that a person starts saving impact the amount they can earn in compound interest.

Why Young Investors Have an Advantage

Younger investors benefit from:

- Longer investment horizon

- Higher risk tolerance

- Lower financial responsibilities

- Smaller opportunity cost

Even small amounts like $50–$100 monthly can grow into significant sums over decades.

The Snowball Effect of Compound Interest

Compound interest works like a snowball rolling downhill.

At first:

- It moves slowly.

- It looks small.

Over time:

- It gathers momentum.

- It grows larger and faster.

The earlier the snowball starts rolling, the bigger it becomes.

Financial Freedom and Early Saving

Starting early doesn’t just increase total money — it increases options.

With strong compound growth, individuals may:

- Retire early

- Work part-time

- Pursue passion projects

- Avoid debt stress

Age determines flexibility.

Lessons from Financial Experts

Many financial experts emphasize:

- Start early.

- Stay consistent.

- Avoid emotional investing.

- Let time do the heavy lifting.

The biggest regret most retirees share is not starting earlier.

Practical Tips to Start Saving Early

If you’re young:

- Open an investment account.

- Automate monthly savings.

- Invest in diversified funds.

- Reinvest dividends.

If you’re older:

- Increase contribution rate.

- Reduce high-interest debt.

- Stay invested long-term.

- Avoid panic selling.

Final Answer: How Does the Age That a Person Starts Saving Impact the Amount They Can Earn in Compound Interest?

The age at which a person starts saving has a dramatic and exponential impact on the amount they can earn in compound interest.

Starting early:

- Multiplies wealth.

- Reduces financial stress.

- Increases long-term options.

- Requires less monthly effort.

Starting late:

- Requires higher contributions.

- Reduces total compounding years.

- Limits growth potential.

Time is the most powerful ingredient in wealth building. You cannot buy more time — you can only use it wisely.

Conclusion

Compound interest rewards patience, discipline, and — most importantly — time. The earlier someone begins saving, the more extraordinary the results can be.

Even small savings started at age 20 can outperform larger savings started at age 35.

The difference isn’t just years — it’s exponential growth.

If there is one financial lesson that stands above all others, it is this:

Start now. Start small. But start early.

Because when it comes to compound interest, age is not just a number — it is the engine that drives wealth.